Anthropic Valuation: $4B Amazon Deal & $1B Zoom Stake Explained

⚡ Quick Take

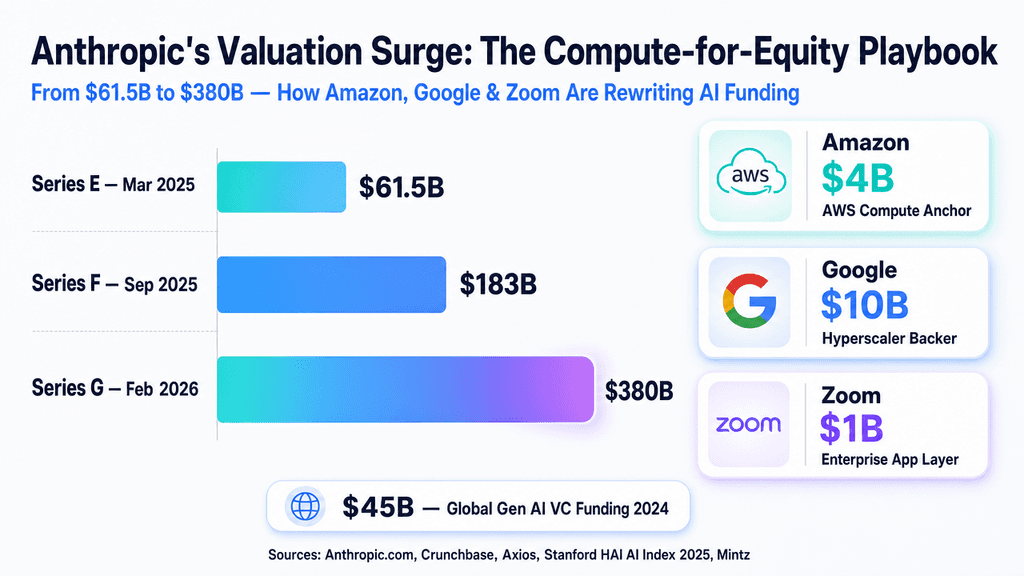

Anthropic’s ballooning valuation, fueled by a $1 billion stake from Zoom and a $4 billion hyperscaler pact with Amazon, is cementing the AI lab’s position as a heavyweight alternative to the Microsoft-OpenAI alliance. These capital injections are rewriting how intelligence is distributed, traded, and hosted.

Summary

Zoom’s swelling $1 billion stake and Amazon’s massive $4 billion commitment highlight Anthropic’s escalating valuation and its strategy of assembling a diverse coalition of hyperscalers and enterprise application distributors. Rather than tying itself to a single cloud monolith, the maker of the Claude model is weaving a web of strategic alliances to secure capital, compute, and market access.

What happened

Video conferencing giant Zoom reportedly increased its investment in Anthropic to roughly $1 billion, following a landmark deal in which Amazon committed up to $4 billion. The Amazon deal deeply binds Anthropic’s generative AI models to AWS infrastructure, integrating them natively into the Bedrock platform and committing Anthropic to use custom AWS silicon.

Why it matters now

The LLM race is no longer just about parameter counts or benchmark scores; it’s a capital-intensive battle for compute dominance and distribution lock-in. Anthropic is successfully securing both the hard cash and the guaranteed chip supply needed to train next-generation models while locking in massive enterprise revenue channels through AWS and Zoom.

Who is most affected

Enterprise IT buyers selecting foundational models to build upon, cloud providers (AWS, Google Cloud) battling to host the heaviest AI workloads, and rival foundational model labs needing to secure their own strategic computing pipelines.

The under-reported angle

Mainstream news isolates these investments as traditional venture rounds, missing the fact that these deals heavily blur the lines between equity, cloud lock-in, and compute credits. Amazon’s investment acts as a demand engine for its own custom Trainium and Inferentia chips, effectively turning Anthropic into a marquee tenant that validates the cloud provider’s non-NVIDIA supply chain.

🧠 Deep Dive

Have you ever wondered how quickly the ground shifts once cloud giants start trading equity for hardware commitments? The recent revelation that Zoom’s stake in Anthropic has mushroomed to $1 billion marks a structural shift in AI market dynamics. While mainstream tech coverage fixates on rapid valuation surges and cash totals, the underlying mechanics reveal a much more complex ecosystem. Anthropic isn’t merely raising capital; from what I’ve seen, it is brokering intelligence in exchange for downstream distribution and upstream infrastructure. Zoom’s expanded footprint illustrates how application-layer giants are scrambling for preferential, deep-tier access to top LLMs to power their AI copilots and enterprise features without depending entirely on OpenAI.

But the heavier anchor in Anthropic’s cap table remains the hyperscalers. Amazon’s $4 billion injection - alongside Google’s continued backing - sets up a multi-front proxy war against the Microsoft-built moat around OpenAI. As noted in the breakdown of the Amazon deal, this capital comes with profound infrastructural strings attached. Amazon’s investment explicitly requires Anthropic to leverage AWS Trainium and Inferentia chips for future model training and deployment.

This creates an inescapable compute-for-equity feedback loop. It is the ultimate cloud lock-in mechanism: funding a model builder with billions, only to have a significant portion of that capital immediately recycled back into the investor’s own compute infrastructure. For Anthropic, this solves a critical pain point - guaranteed access to scarce training hardware amid global GPU supply bottlenecks. For Amazon, it turns the Claude model family into a killer app for AWS Bedrock, while finally validating its proprietary, non-NVIDIA silicon roadmap to the broader enterprise market.

Yet this intricate web of strategic dependencies introduces obscured risks that regulatory watchdogs are only just beginning to scrutinize. With AI cap tables increasingly dominated by cloud providers trading compute credits in lieu of hard cash, traditional valuation multiples are distorted. As Anthropic pushes forward with its "constitutional AI" and safety-first mission, its escalating reliance on hyperscaler margins and hardware roadmaps will test whether an independent governance structure - like its Long-Term Benefit Trust - can survive the sheer financial gravity of AI infrastructure demands.

📊 Stakeholders & Impact

- AI / LLM Providers — High impact. Forces competitors (OpenAI, Cohere) to aggressively secure their own strategic distribution and compute pipelines as capital requirements for next-gen training soar.

- Infrastructure & Clouds — Critical. Transforms leading AI startups into captive R&D drivers for custom silicon (Trainium, TPUs) and guarantees massive, sticky cloud consumption.

- Enterprise App Ecosystem — High. Companies like Zoom secure priority API access and co-development alignment, embedding Claude directly into high-value B2B workflows.

- Regulators & Policy — Significant. Sparks scrutiny over whether "compute-for-equity" structures are backdoor monopolies bypassing traditional M&A reviews.

✍️ About the analysis

This independent analysis synthesizes commercial investment reports, hyperscaler press releases, and structured cap-table data to decode the evolving mechanics of AI funding. Designed for infrastructure strategists, cloud architects, and enterprise decision-makers, it bypasses the valuation hype to expose the physical and economic lock-ins driving the LLM market.

🔭 i10x Perspective

The Anthropic investment saga proves that standalone LLM companies max out quickly without deep, structural integration into the physical layer of the internet. By playing Amazon, Google, and Zoom off each other, Anthropic has uniquely avoided subservience to a single master, attempting to weaponize cloud competition to its own advantage. Over the next five years, I suspect the critical metric determining AI market supremacy won’t be private valuation, but who controls the silicon pipeline - and whether these closed compute-funding loops trigger aggressive antitrust intervention.

Related News

Grok Imagine Odyssey: xAI's Long-Form Video Ambitions

Elon Musk announced Grok Imagine for a full-length, historically accurate Odyssey film. Explore the massive AI infrastructure and temporal consistency challenges this project presents. Learn more.

xAI Grok 4.5 & 4.6: Tavily Integration Cuts Hallucinations

xAI moved Grok web retrieval to Tavily 4 for sharper reasoning and fewer errors. See how this modular approach affects developers, benchmarks, and future model scaling. Learn more.

Kimi K3: Moonshot AI Builds Frontier LLM With Limited Hardware

Moonshot AI's Kimi K3 delivers strong reasoning, coding, and ultra-long context under hardware limits. It gives Chinese enterprises a compliant high-performance option. Explore the analysis.