Enterprise AI Consolidation: From Sprawl to Core Portfolios

Enterprise AI Consolidation: From Sprawl to Core Portfolios

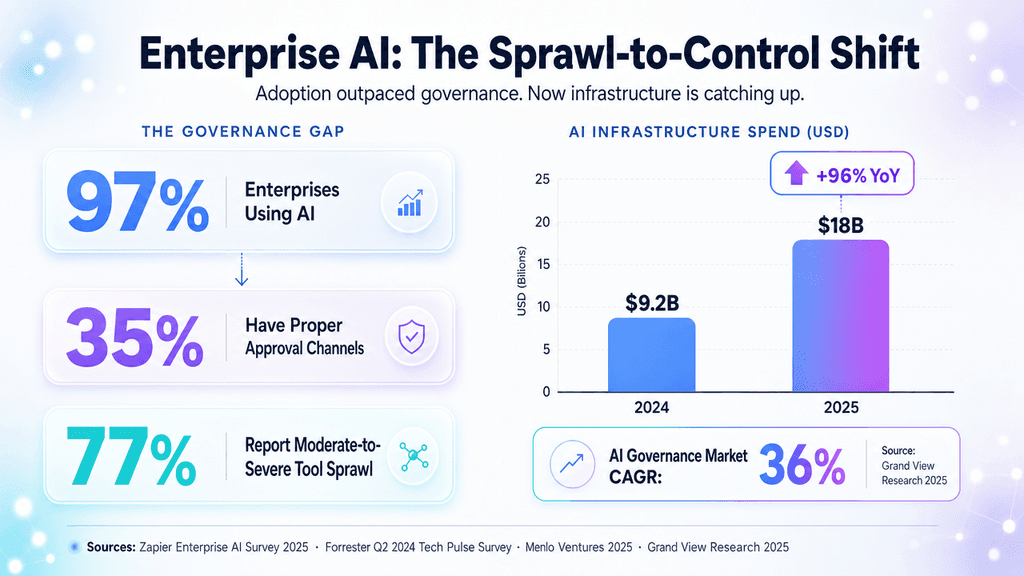

Summary: The unpredictable "Wild West" phase of enterprise AI experimentation is winding down fast. Organizations are shifting from dozens of scattered LLMs to a tightly managed set of one to three core models under proper governance.

What happened: Skyrocketing inference costs, compliance gaps, and outright model sprawl have prompted CIOs and platform teams to retire redundant models and roll out centralized evaluation and routing systems.

Why it matters now: This consolidation wave is reshaping the AI infrastructure market. Budgets and attention are moving away from raw model power and toward Total Cost of Ownership (TCO), latency SLOs, and unified observability.

Who is most affected: CFOs working to control cloud spending, platform engineers building unified AI gateways, and tier-two model providers at risk of losing their place in enterprise stacks.

The under-reported angle: The quiet tension between consolidation and vendor lock-in. Companies want fewer models to manage, yet they’re also investing in new portability layers and dynamic routing to keep their options open.

🧠 Deep Dive

Ever wonder why the flood of AI pilots suddenly feels harder to sustain? The era of “bring your own LLM” is running into corporate reality. For the past year, teams have spun up everything from on-premises Llama instances to direct GPT-4 pipelines just to test isolated ideas. Recent reports from McKinsey and Forbes show the result: a messy mix of model sprawl, unpredictable spending, and governance that’s spread too thin.

Faced with overlapping tools and murky returns, enterprises are standardizing on a small “core portfolio.” Usually that means one frontier model for tough reasoning tasks and one or two leaner, cheaper models for everyday work. CTOs are mapping capabilities, spotting duplicates, and phasing out the rest.

Infrastructure providers are moving quickly to meet this demand. Platforms like Databricks Mosaic AI and AWS Bedrock now pitch “consolidation-as-a-service,” complete with central registries, shared evaluation tools, and policy controls that let engineers hide complexity behind one manageable endpoint. Their goal is clear: own the control plane so every request passes through their cost and risk checks.

This shift is also a compliance move. CISOs need reliable data provenance for GDPR, HIPAA, and upcoming AI rules, and it’s nearly impossible to enforce across fifteen separate, ungoverned deployments. Consolidation gives them the audit trail they need.

Still, trimming too aggressively creates its own risk. Betting everything on one vendor can lead to painful lock-in. That’s why forward-thinking teams are adding intelligent routing layers and light A/B testing instead of rigid single-model rules. The real consolidation, then, isn’t just deleting models—it’s abstracting them so thoroughly that business users no longer notice or care which one is doing the work.

📊 Stakeholders & Impact

Stakeholder / Aspect | Impact | Insight |

|---|---|---|

Core LLM Providers | High | A “winner-takes-all” pattern is forming; the models that land in the core portfolio secure steady, high-volume inference revenue. |

Tier-2 & Niche Models | Negative | Secondary models are likely to be cut unless they show clear specialized value or much lower TCO. |

Platform & Cloud Infra | High | Cloud platforms (AWS, Databricks) stand to gain by supplying the routing, observability, and governance layers that tame sprawl. |

CFOs, CIOs & CISOs | Significant | Improved visibility into cost per 1k tokens, faster risk reduction, and direct mapping of usage to compliance controls. |

✍️ About the analysis

This independent analysis draws on current market signals, consulting frameworks, and infrastructure vendor plans around enterprise AI. It aims to give CTOs, platform engineers, and AI leaders a practical picture of the changing economics and governance requirements.

🔭 i10x Perspective

The move toward fewer LLMs shows how quickly AI is settling into ordinary IT infrastructure. As enterprises narrow their choices, the center of gravity shifts from model creation to the routing and middleware layer. Over the next three to five years, the most valuable investments will likely sit in the intelligent fabrics that route prompts according to real-time token cost, latency needs, and governance policies. The models themselves are becoming more interchangeable; the orchestration layer is where lasting advantage will be built.

Related News

Grok Imagine Odyssey: xAI's Long-Form Video Ambitions

Elon Musk announced Grok Imagine for a full-length, historically accurate Odyssey film. Explore the massive AI infrastructure and temporal consistency challenges this project presents. Learn more.

xAI Grok 4.5 & 4.6: Tavily Integration Cuts Hallucinations

xAI moved Grok web retrieval to Tavily 4 for sharper reasoning and fewer errors. See how this modular approach affects developers, benchmarks, and future model scaling. Learn more.

Kimi K3: Moonshot AI Builds Frontier LLM With Limited Hardware

Moonshot AI's Kimi K3 delivers strong reasoning, coding, and ultra-long context under hardware limits. It gives Chinese enterprises a compliant high-performance option. Explore the analysis.