European AI Sovereignty vs US Hyperscalers Reality

Summary

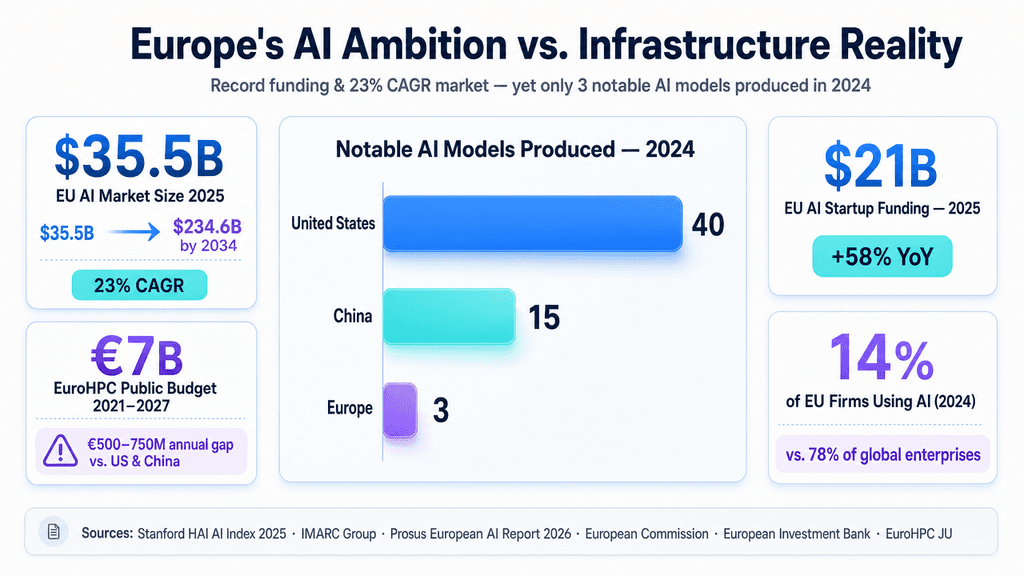

While traditional market reports project massive growth for the European AI sector through 2030, the underlying infrastructure tells a more complex story of European LLM champions relying heavily on US hyperscaler compute.

Europe is rapidly scaling its AI ecosystem, driven by an influx of capital into generative AI startups, the formalization of the EU AI Act, and heavy public investment in EuroHPC supercomputers.

The narrative of "Sovereign European AI" is colliding with the physical reality of the GPU supply chain; leading local models are heavily intertwined with US cloud infrastructure, dictating how AI is actually built and distributed across the continent.

European enterprise buyers (CTOs, procurement), sovereign cloud providers (OVHcloud, Scaleway), US hyperscalers (AWS, Azure), and AI model builders navigating new compliance parameters are among the most affected stakeholders.

Most commercial forecasts ignore the "dependency atlas" of European AI—specifically how the push toward open-source models is being used as a strategic wedge by local enterprises to avoid cloud lock-in and manage AI Act compliance costs.

Deep Dive

Sovereignty vs. Practicality

Have you ever wondered why the numbers in syndicated reports feel a touch too clean? If you read the standard market forecasts, the European AI ecosystem sounds like a straightforward upward curve of software, hardware, and services spending through 2032. Yet beneath those competitive landscapes and generic adoption drivers sits a far more fragmented reality. Europe's AI market is shaped less by tidy geographic growth and more by the ongoing tension between sovereign intelligence goals and a deep reliance on US hyperscaler infrastructure.

The real story is the "Sovereignty vs. Practicality" debate. European tech policy pushes hard for digital independence, but the continent's standout AI exports remain tied to cross-Atlantic partnerships. Mistral’s distribution alignments and DeepL’s operational reliance on AWS show a simple fact: scaling foundational models today demands compute density that local providers like OVHcloud or Scaleway are still working to match. For now, most European AI runs on American hardware, even when housed in local data centers to meet residency rules.

To ease this bottleneck, Europe is turning to public infrastructure and regulation. The EuroHPC Joint Undertaking, with systems like LUMI in Finland and Leonardo in Italy, aims to give researchers and startups a non-commercial GPU path. Still, moving from those public clusters to reliable commercial capacity creates real friction. In parallel, enterprises are leaning toward open-weight models and open-source derivatives such as LLaMA variants and Mixtral. This choice is often less about ideology and more about managing total cost of ownership—allowing firms in Germany and France to fine-tune models on-premise or in controlled environments.

Regulation adds another filter. Rather than treating the EU AI Act purely as a constraint, many vendors now position "trust-by-design" and data minimization as selling points. That approach is speeding demand for vertical-specific models in healthcare and finance. As a result, the European market is moving away from the US-style race for ever-larger frontier models and toward smaller, compliant systems that can handle its multilingual realities.

Stakeholders & Impact

- European AI Builders — High impact: Companies like Mistral and Aleph Alpha must balance "sovereign" brand positioning with the practical need to partner with US tech giants for compute and distribution.

- US Cloud Hyperscalers — High impact: AWS, Azure, and GCP provide the foundational infrastructure for Europe's AI boom, but face increasing pressure to prove data residency and regulatory isolation.

- Enterprise Buyers — Medium–High impact: Budgets are shifting toward open-source models and hybrid deployments to control ROI, avoid vendor lock-in, and integrate natively into existing European ERP/MES stacks.

- Regulators & Policymakers — Significant impact: Authorities are forcing global players to adapt to the AI Act while simultaneously trying to scale EuroHPC to reduce long-term structural dependency on foreign tech.

About the analysis

This independent analysis draws on commercial market intelligence, VC funding benchmarks from Atomico and Dealroom, and current tech policy developments. It is meant for enterprise decision-makers, CTOs, and AI strategists who need a clearer picture of infrastructure dependencies, regulatory constraints, and realistic procurement options.

i10x Perspective

Europe isn't losing the AI race; it is optimizing for a different endgame. By leaning into open-weight models and treating the AI Act as a baseline, the continent is putting enterprise integration, localized safety, and domain-specific intelligence ahead of raw scaling. The key question over the next five years is whether local compute providers and the EuroHPC network can grow fast enough to offer a genuine alternative before the next wave of agentic systems arrives.

Related News

Grok Imagine Odyssey: xAI's Long-Form Video Ambitions

Elon Musk announced Grok Imagine for a full-length, historically accurate Odyssey film. Explore the massive AI infrastructure and temporal consistency challenges this project presents. Learn more.

xAI Grok 4.5 & 4.6: Tavily Integration Cuts Hallucinations

xAI moved Grok web retrieval to Tavily 4 for sharper reasoning and fewer errors. See how this modular approach affects developers, benchmarks, and future model scaling. Learn more.

Kimi K3: Moonshot AI Builds Frontier LLM With Limited Hardware

Moonshot AI's Kimi K3 delivers strong reasoning, coding, and ultra-long context under hardware limits. It gives Chinese enterprises a compliant high-performance option. Explore the analysis.