Starlink Enables Decentralized AI Infrastructure via Remote Data Centers

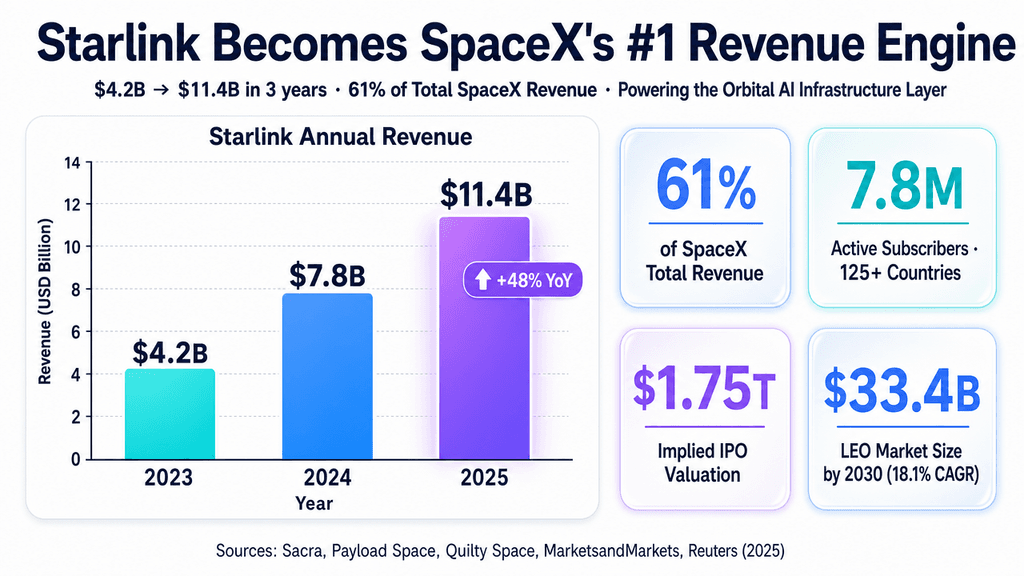

SpaceX’s Starlink has officially overtaken traditional launch services to become the company’s primary revenue engine ahead of a highly anticipated, record-breaking IPO.

Summary: While traditional financial markets view this strictly as a telecommunications and aerospace milestone, the shifting unit economics of space connectivity deeply alter the future of decentralized AI infrastructure.

What happened: Recent market intelligence reveals that Starlink’s high-margin segments—particularly enterprise, mobility, and government backhaul—are now driving the majority of SpaceX’s rapidly scaling revenue. This financial maturation is prepping the ground for what could be one of the largest tech IPOs in history, proving that LEO (Low Earth Orbit) constellations are financially viable at a massive scale.

Why it matters now: The LLM training and inference race is hitting a hard physical bottleneck: grid capacity. As builders look to house multi-gigawatt AI training clusters in remote locations to tap into "stranded power" (like off-grid desert solar or remote nuclear), traditional fiber isn't always viable. High-throughput, low-latency LEO networks are the critical backhaul required to sync remote AI data centers with end-user inference hubs.

Who is most affected: Hyperscalers (AWS, Google, Microsoft) exploring remote data center deployments, edge AI developers building autonomous hardware, and incumbent terrestrial telecom providers unequipped to handle global, decentralized AI workloads.

The under-reported angle: Traditional coverage views Starlink’s soaring ARPU (Average Revenue Per User) through a telecom lens, missing the strategic cross-pollination in Elon Musk's empire. Starlink’s massive free cash flow is the ultimate sovereign wealth engine subsidizing massive GPU procurement, while its network creates the global nervous system required to deploy autonomous agents and real-time physical AI anywhere on Earth.

🧠 Deep Dive

Have you ever stopped to wonder why the AI build-out keeps running into walls that look more like power lines than code limits? The narrative surrounding SpaceX’s expected record IPO is currently dominated by subscriber momentum and aerospace supremacy. Yet, beneath the standard financial metrics—EBITDA margins, ARPU, and terminal payback—lies a quiet but fundamental shift in computing architecture.

From what I've seen, as Starlink transitions from a rural broadband band-aid to a profitable, high-bandwidth enterprise backhaul network, it is inadvertently solving one of the core infrastructure crises facing artificial intelligence: geographic constraint. Right now, the AI industry is running out of urban power. Major infrastructure players are scouring the globe for stranded power—massive gigawatt energy pockets isolated from main grids and traditional fiber trunk lines. An LLM training facility positioned next to a remote hydro-dam or geothermal plant requires exorbitant, multi-year fiber trenching to connect to the broader internet. Starlink’s maturing enterprise footprint provides an immediate, deployable data bridge for these off-grid AI data centers, shifting the economics of where supercomputers can actually be built.

Furthermore, as AI transitions from chat interfaces to autonomous agents functioning in the physical world (robotics, drones, and self-driving fleets), continuous edge-to-cloud inference is non-negotiable. Starlink’s dominance in mobility and geographic reach establishes a planetary-scale mesh network. Without this LEO backhaul, physical AI models face severe latency and deployment limits outside of dense urban corridors. Starlink's network utilization is essentially becoming the delivery mechanism for ubiquitous AI inference.

This revenue surge also signals the opening of a new competitive front in the cloud wars. It is no coincidence that Amazon is aggressively pushing its own LEO constellation, Project Kuiper. AWS understands that owning the orbital backhaul is the final piece of end-to-end proprietary infrastructure. To compete against SpaceX’s head start, Kuiper and other incumbent network providers will need to offer heavily subsidized capacity, directly bundling cloud inference with space backhaul.

Ultimately, Starlink’s unit economics—leveraging in-house launch cadences to aggressively lower the capital expenditure per gigabit of sellable throughput—creates an unsurpassable moat. The massive cash flow derived from diverse revenue models (maritime, aviation, and government defense) doesn't just promise a historic IPO. It builds a self-funding intelligence loop where space revenue secures the capital necessary to buy compute, train frontier models, and deploy them across a globally owned terrestrial and orbital network.

📊 Stakeholders & Impact

Stakeholder / Aspect | Impact | Insight |

|---|---|---|

AI / LLM Cloud Providers | High | LEO constellations enable strategic decoupling from urban power grids by providing backhaul for remote, stranded-energy AI data centers. |

Edge AI & Autonomous Systems | High | Physical AI agents and fleets gain the required low-latency, uninterrupted global connectivity for real-time inference. |

Incumbent Telecoms | Severe | Traditional terrestrial providers face eroding enterprise ARPU and backhaul relevance as mega-constellations mature. |

Investors & xAI Ecosystem | Significant | Starlink's IPO and cash flow provide massive capital leverage, enabling sustained heavy GPU capex without external equity dilution. |

✍️ About the analysis

This independent analysis synthesizes incoming telecom revenue and IPO capitalization signals, mapping them against the urgent power and connectivity constraints currently reshaping the AI and ML infrastructure ecosystem. It is designed for CTOs, AI hardware architects, and infrastructure strategists tracking the convergence of space tech and compute scalability.

🔭 i10x Perspective

Starlink’s impending ascendancy via a record IPO is proof that intelligence infrastructure is moving entirely off-grid. Over the next decade, the companies that control the orbital layer will dictate the terms of physical AI deployment, essentially charging a toll for every autonomous agent and remote data center that needs to phone home. We are no longer just looking at a satellite ISP; we are watching the construction of the planetary nervous system that will carry the weight of post-AGI global inference.

Related News

Grok Imagine Odyssey: xAI's Long-Form Video Ambitions

Elon Musk announced Grok Imagine for a full-length, historically accurate Odyssey film. Explore the massive AI infrastructure and temporal consistency challenges this project presents. Learn more.

xAI Grok 4.5 & 4.6: Tavily Integration Cuts Hallucinations

xAI moved Grok web retrieval to Tavily 4 for sharper reasoning and fewer errors. See how this modular approach affects developers, benchmarks, and future model scaling. Learn more.

Kimi K3: Moonshot AI Builds Frontier LLM With Limited Hardware

Moonshot AI's Kimi K3 delivers strong reasoning, coding, and ultra-long context under hardware limits. It gives Chinese enterprises a compliant high-performance option. Explore the analysis.